The Tax Bill Beneath

the Tax Bill

How special districts — MUDs, PIDs, ESDs, and others — can add hundreds of dollars to your monthly housing cost, whether you are buying new construction or a ten-year-old resale. Written from someone who learned it the hard way.

Range in Hill Country

Special Districts Can Add

Taxing Districts

Repayment Term

In This Guide

Five years ago, when I moved to the Texas Hill Country, I thought I understood property taxes. I'd spent nearly four decades in high-tech sales and marketing — I knew how to read a balance sheet, how to negotiate a deal, and how to do my homework before making a major decision. But nothing in my background had prepared me for what I encountered with Texas property taxing authorities.

I'd never heard of a MUD or a PID. I had no idea that the property tax rate on a listing sheet could be missing entire layers of cost. Almost every buyer relocating to the Hill Country has the same gap in their understanding, and the consequence is expensive: a tax bill that can be thousands of dollars higher than what the listing suggested.

Here's the scenario I see play out again and again. You find the right home in the Texas Hill Country — maybe it's a brand-new build in a master-planned community, or maybe it's a well-maintained ten-year-old resale in a neighborhood you love. The listing price fits your budget. The property tax estimate on the listing sheet looks manageable — maybe $6,500 a year. Everything checks out. Then you close. Months later, the first full tax bill arrives. The number is not $6,500. It is $11,200. Your monthly housing payment just jumped by $390 — and you have no idea why. Hypothetical illustration

That experience is why I wrote this article. This is everything I've learned about special taxing districts in the Texas Hill Country, written out so you don't have to go through the same discovery process I did.

What follows is a thorough explanation of what these districts are, how they work, and how to calculate their impact on your monthly payment before you sign a purchase contract. Whether you're buying brand-new construction or a resale, this is the article that saves you from an expensive surprise.

Special taxing districts do not only affect new construction. Established resale homes in Hill Country neighborhoods carry the same ongoing tax obligations.

Key Takeaway

- •The property tax rate on a home is not a single number — it is a composite of county, school district, city, and special district levies.

- •Special districts (MUDs, ESDs, and others) can add $0.50 to $1.50 or more per $100 of taxable value on top of the base tax rate — for both new construction and resale homes. PIDs add separate special assessments (annual installments plus interest) rather than ad valorem taxes — the actual amount depends on the apportionment method in the property's Service and Assessment Plan.

- •That layered cost translates to $200 to $500+ per month in additional housing costs on a typical Hill Country home.

- •You can and should identify these districts before you make an offer — regardless of whether the home is new or resale.

Why the Seller's Tax Bill May Not Be Your Tax Bill

The seller's tax bill reflects their exemptions, their capped appraised value, and their specific assessment history — none of which transfer to you as the buyer.

- •Homestead appraisal cap: If the seller has lived in the home for years, their appraised value may be capped well below current market value (up to 10% annual increase from the year they qualified). You will not inherit the seller's capped appraised value. For planning purposes, use the CAD's current market value rather than the seller's capped appraised value. The CAD will determine the property's value for the applicable tax year as of January 1.

- •Over-65 exemption: If the seller is 65 or older, they may have a school district tax ceiling — a maximum dollar amount that prevents their school tax from rising. You will not inherit that ceiling.

- •Disabled-person or disabled-veteran exemption: The seller may receive additional exemptions based on disability status — each requiring separate eligibility and application. These do not carry over.

- •Agricultural or wildlife valuation: If the seller's land qualifies for ag-use or wildlife management valuation, their appraised value is based on productive use — not market value. That valuation likely does not apply to you as a residential buyer. Changing the land's use can also trigger roll-back taxes — a three-year recapture of the difference between taxes based on productivity value and taxes based on market value; penalties and interest may apply if the resulting bill becomes delinquent.

The buyer's tax burden will be calculated on a different basis. Use the tax bill to identify which entities tax the property and their rates, then apply those rates to the CAD's current market value (not the seller's capped appraised value) minus your own exemptions. See How to Estimate Your Actual Tax Bill for the step-by-step method.

How Texas Property Tax

Actually Works

Texas has no state income tax. What most people don't realize is that the absence of income tax is the primary reason property taxes exist at the levels they do. Property tax is not a side effect of homeownership in Texas — it is the primary funding mechanism for local government, public schools, roads, and emergency services.1

The numbers are straightforward: Texas combined property tax rates typically range from 1.5% to 2.5% of assessed value, and in areas with special taxing districts, the combined tax rate can climb to 3.0% or higher.1 That is two to three times what most California buyers are accustomed to paying.

But the rate you see on a listing — or the one a builder quotes on a price sheet — is rarely the full picture. Understanding why requires understanding how the rate is assembled.

Combined Tax Rate vs. Effective Tax Rate

When a listing says a home has a "tax rate of 2.1%," that number is a combined tax rate — the sum of every taxing jurisdiction's adopted rate, added together. It includes the county rate, the school district rate, the city rate, and any special district ad valorem rates (MUD, ESD, and so on), all stacked on top of one another. PID assessments — which are special assessments, not ad valorem taxes — may appear separately and are not included in the combined tax rate figure.

The effective tax rate (total taxes paid as a percentage of market value) is different — it accounts for exemptions and appraisal caps, so it is almost always lower than the combined rate. A $500,000 home paying $10,000 in total taxes has an effective rate of 2.0% even if the combined rate is 2.4%. Hypothetical illustration

The combined tax rate emerges from the overlap of multiple independent taxing authorities, each with its own rate-setting process and bond obligations.

How Jurisdictions Layer

Every property in Texas is taxed by a combination of overlapping entities — not one entity, but several, all at once:

- County — funds county government, roads, courts, and general services. Typically $0.20 to $0.40 per $100 of taxable value.2

- School District — the largest single component of most tax bills, funding K–12 education. Rates typically range from $0.80 to $1.15 per $100 depending on the district.3

- City (if within city limits) — funds municipal services. Can range from $0.20 to $0.65 per $100.

- Special Districts — MUDs, ESDs, WCIDs, road districts, and others levy ad valorem taxes. PIDs, which are created by a city or county rather than existing as independent taxing authorities, add special assessments rather than ad valorem taxes. These are the layers this article focuses on, and they are where most of the cost surprise lives.

A home inside Boerne city limits, for example, might be taxed by Kendall County, Boerne ISD, the City of Boerne, and one or more special districts — all simultaneously. A home five miles outside city limits might skip the city tax but pick up an ESD and a MUD instead. The combined tax rate can be quite different, even within the same county. Hypothetical illustration

The layers of taxing jurisdictions that stack onto every Hill Country property tax bill. Special districts (MUD, ESD) sit on top of the base county, school, and city levies. PIDs add special assessments — not ad valorem taxes — as an additional cost.

Key Takeaway

Your property tax rate is the sum of every overlapping jurisdiction — not a single number set by one entity. Special districts are additional layers that sit on top of the base county and school district rates, and they can double or triple the impact on your monthly payment.

Special Districts — The Layers

Beneath Your Tax Bill

Texas has more than 2,300 special purpose districts that levy property taxes.4 These are independent government entities created to fund specific services — water infrastructure, roads, emergency response, drainage — that the county or city does not cover on its own. In new-growth areas like the Hill Country, special districts are not unusual. They are the standard mechanism for financing the infrastructure that makes a new subdivision possible.

Here are the five types most likely to appear on a Hill Country tax bill.

MUD — Municipal Utility District

Most common in new Hill Country developments

MUDs fund the core infrastructure a new subdivision needs: water supply lines, wastewater and sewer systems, stormwater drainage, and roads.

A Municipal Utility District is an independent political subdivision created to finance and maintain water supply, wastewater treatment, drainage, and road infrastructure for a specific development or geographic area.5 In the Hill Country, where there is no existing municipal water or sewer system, a MUD is typically the vehicle used to fund the infrastructure.

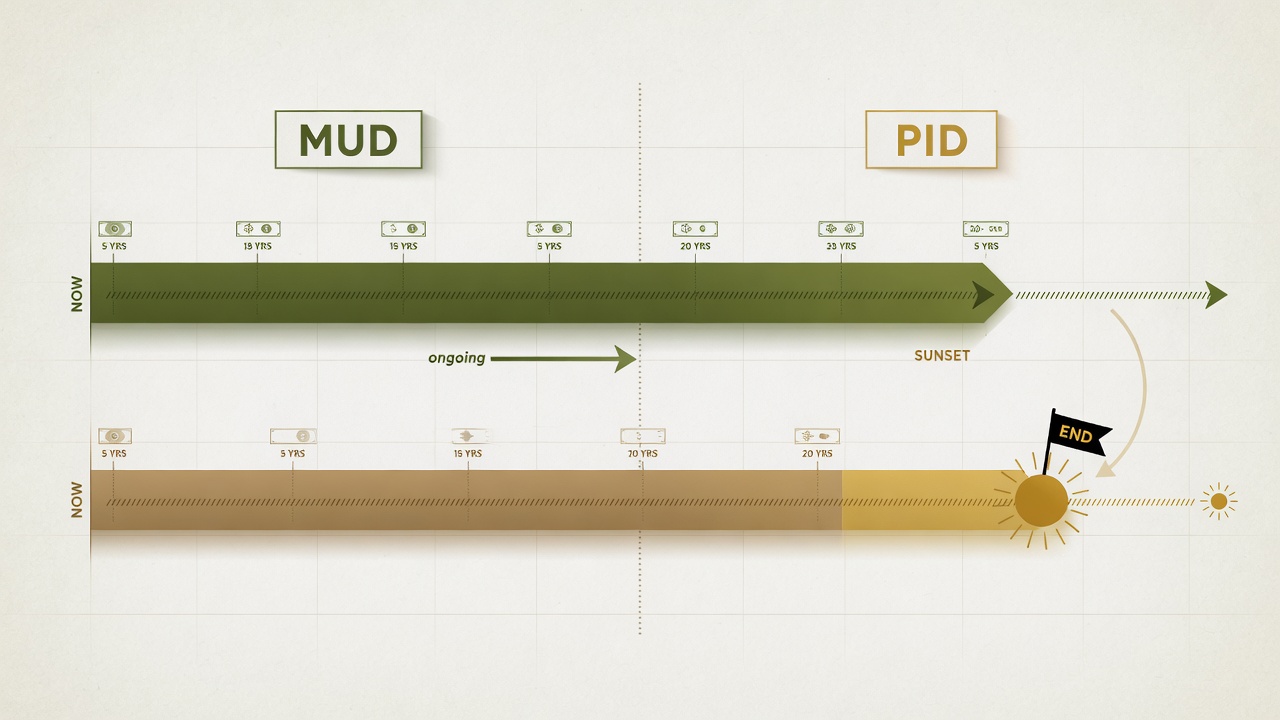

Here is how it works: The developer pays upfront to build water lines, sewer systems, roads, and drainage. The MUD then issues tax-exempt municipal bonds to reimburse the developer for those costs. The bond debt is repaid over 20 to 30 years through a property tax levied on every homeowner within the district.6

MUD tax rates typically range from $0.25 to $1.50 per $100 of taxable value, depending on the amount of bond debt outstanding and the infrastructure being maintained.7 On a $750,000 home with no applicable exemptions, that translates to an additional $1,875 to $11,250 per year — on top of the county, school, and city taxes.

MUD Rate Breakdown: M&O vs. I&S

A MUD typically levies two separate tax rates that combine into the total MUD rate you see on your tax bill. Understanding the difference matters — especially when estimating how your tax burden will change over time.

Maintenance & Operations (M&O) rate — Funds day-to-day operations: water treatment, sewer maintenance, infrastructure upkeep, and administrative costs. It does not go away when bonds are paid off.

Interest & Sinking (I&S) rate — Also called the debt service rate. This repays the bonds issued to fund initial infrastructure. The I&S rate may decline as debt is retired and can reach zero when all bonds are retired, assuming no new bonds are taken on.

The total MUD tax rate is M&O + I&S. Early in a district's life, the I&S portion is typically larger. As bonds mature, only the I&S portion is affected — and whether the total rate actually declines depends on the repayment schedule and new debt issuance.

Example: Hypothetical illustration A MUD with a total rate of $1.25 per $100 might have a $0.45 M&O rate and a $0.80 I&S rate. When bonds are paid off, the I&S rate drops to zero — but the $0.45 M&O rate remains. "Bonds paid off" does not mean no more MUD tax.

See How Bond Debt Turns Into Your Monthly Payment for how this translates to your monthly cost.

MUD utility charges are separate from property taxes. MUDs often provide water and sewer service directly — these charges appear on a separate bill and are not part of the ad valorem tax. Budget for both the MUD property tax and the MUD utility charges.

PID — Public Improvement District

Created by a city or county — not an independent taxing authority

PIDs can fund a broad range of public improvements — from infrastructure like roads, drainage, and utilities to neighborhood enhancements such as parks, landscaping, lighting, sidewalks, and trails.

A Public Improvement District is a defined geographic area — created by a city or county — where property owners pay a special assessment (not a traditional property tax) to fund public improvements including infrastructure, parks, landscaping, lighting, sidewalks, and trail systems.8 Unlike a MUD, a PID is not an independent taxing authority — it does not levy ad valorem property taxes.

PID assessments are typically structured as annual installments plus interest, rather than a single lump sum. Texas law permits assessments to vary annually, and outstanding balances may be prepaid. There is no dependable statewide typical PID rate — Texas law allows costs to be apportioned using different methods based on special benefit, including frontage, square footage, property value, or other formulas. To determine the specific amount that applies to your property, consult the property's actual assessment roll and the PID's current Service and Assessment Plan.

A PID may include capital assessments for infrastructure, bond installments tied to a repayment schedule, and ongoing service or maintenance assessments for landscaping, security, or common-area upkeep — each with its own duration. Ongoing service assessments may have no fixed expiration at all. See PID Due Diligence Checklist for the documents to request.

WCID — Water Control and Improvement District

Water supply, flood control, and drainage

WCIDs manage water supply, flood control, stormwater drainage, and sometimes wastewater — particularly important in the Hill Country where karst topography and flash-flood geography demand complex water management.

A Water Control and Improvement District manages water supply, flood control, stormwater drainage, and sometimes wastewater for a specific area.9 WCIDs are particularly common in the Hill Country, where the Edwards Aquifer (Edwards Aquifer Authority — learn more), karst topography (USGS overview — learn more), and flash-flood geography create complex water management challenges.

WCIDs function similarly to MUDs in that they can issue bonds and levy property taxes to repay them. In some developments, a WCID and a MUD may overlap — meaning homeowners pay taxes to both entities. The tax rate for a WCID typically falls in the range of $0.10 to $0.50 per $100 of taxable value, though this varies with the scope of infrastructure managed.

ESD — Emergency Services District

Fire protection and emergency medical services

ESDs fund fire protection and emergency medical services in unincorporated areas — a permanent levy that does not sunset.

An Emergency Services District funds fire protection and emergency medical services in areas outside incorporated city limits.10 ESDs are most common in unincorporated areas — precisely where many Hill Country properties are located.

In Bexar County, ESD tax rates have ranged from approximately $0.06 to $0.10 per $100 of taxable value.10 On a $750,000 home that adds $450 to $750 per year. In some Hill Country areas, ESD rates can be higher.

Unlike MUD taxes and PID assessments, ESD taxes are ongoing levies — they do not sunset when bonds are paid off. They are a permanent layer for as long as the district exists.

Road Utility Districts

Local road construction and maintenance

Road utility districts fund the construction and maintenance of local roads within a defined area, particularly in newer developments where county roads must be built or upgraded.

Road utility districts fund the construction and maintenance of local roads within a defined area, most common in newer developments. Like MUDs, they can issue bonds and levy ad valorem taxes — typically $0.05 to $0.20 per $100 of taxable value, one more layer that compounds the total rate.

"These districts are not inherently harmful. They fund the infrastructure that makes communities possible. The problem is not their existence — it is that most buyers do not know they exist until the first tax bill arrives."

The California Connection:

Mello-Roos and CFDs

If you are relocating from California, the concept of a MUD is not entirely new to you. You've likely encountered a related mechanism — one that most California buyers already pay without thinking twice about it. Understanding the parallels between Texas special districts and California's Mello-Roos/CFD system gives you a significant head start in evaluating your true housing cost in the Hill Country.

California's Closest Analogue to a Texas MUD

California created the Mello-Roos Community Facilities Act of 1982 to address a similar challenge: funding infrastructure for new developments. Under this law, an authorized local agency — such as a county, city, or special district — may form a Community Facilities District (CFD) that issues bonds for roads, schools, water systems, sewer lines, parks, and other public facilities. Homeowners within the CFD pay a special tax to service that bond debt.22

A CFD is California's closest analogue to a Texas MUD, but the mechanisms differ in important ways. A CFD may finance services in addition to infrastructure, imposes a special tax under its own rate and method of apportionment, and is not structured as an independent political subdivision in the same way a Texas MUD is. The overlap is real — both use bond-funded mechanisms to pay for development infrastructure — but the legal frameworks, rate-setting processes, and governance structures are distinct.

How They Compare: Side by Side

The table below maps Texas MUD and PID features alongside their closest California counterparts. The parallels are useful for California relocators, but remember: these are analogies, not direct equivalents.

| Feature | Texas MUD / PID | California Mello-Roos / CFD |

|---|---|---|

| Purpose | Fund infrastructure and public improvements for new development — MUDs cover roads, water, sewer, parks; PIDs may also cover roads, drainage, utilities, and neighborhood enhancements | Fund infrastructure and services for new development — roads, schools, water, sewer, parks, and ongoing public services |

| Duration | 20–30+ years (MUD bonds). PID capital assessments are paid in annual installments plus interest; assessments may vary annually and can be prepaid. Ongoing service/maintenance assessments may continue indefinitely. | 20–30+ years (typical Mello-Roos bond term) |

| Who bears the cost | Every property within the district boundaries | Every property within the CFD boundaries |

| Transfers with property | Yes | Yes |

| Assessed by | MUD: local appraisal district (county), with tax rate set by the district board. PID: administered by the city or county that created it — not an independent taxing authority | County tax collector, based on the CFD's established tax rate |

| Assessment basis — MUD | Taxable value multiplied by adopted MUD rate | — |

| Assessment basis — PID | Allocation method in current Service and Assessment Plan | — |

| Assessment basis — Mello-Roos | — | CFD's adopted rate and method of apportionment |

| Appears on tax bill | MUD: separate line item on tax bill. PID: may appear on the tax bill or on a separate assessment notice. | Yes — separate line item, often labeled "Special Tax" or "CFD" |

| Buyer disclosure required | MUD: Texas Water Code § 49.452. PID: Texas Property Code § 5.014 — written notice required before a binding contract. | Yes — California Civil Code § 1102.6b (seller disclosure); also typically appears in the Preliminary Title Report |

Where They Differ

The parallels are close enough that California buyers have a useful head start — but the differences matter. The legal frameworks, rate-setting methods, and governance structures are not the same, and those distinctions affect how you evaluate a Texas property.

Naming and structure. California calls them "Mello-Roos" or "CFDs." Texas calls them "MUDs," "PIDs," "WCIDs," and others. MUDs and PIDs are structurally different — a MUD is an independent taxing authority that levies ad valorem taxes, while a PID is created by a city or county and imposes special assessments. If someone mentions a "MUD" in a Hill Country listing, it is worth understanding: a Texas MUD is a closer analogy to a California CFD than it is to any single California tax mechanism.

Rate behavior. Critically, California Mello-Roos rates are typically fixed or follow a disclosed escalation schedule, while Texas MUD rates are set annually and can fluctuate. PID assessments are also permitted to vary annually under Texas law.

The Proposition 13 Difference

Texas has no Proposition 13 equivalent. The 10% annual homestead appraisal cap provides less protection than California's 2% lock on purchase price, and non-homestead properties face only a temporary 20% cap (expiring Dec 31, 2026 for properties ≤$5M). This fundamentally changes how you model long-term housing cost. See Why a Lower Rate Doesn't Mean a Lower Bill for the full analysis.

What This Means for You as a Relocator

If you've been paying a Mello-Roos tax in California, you already understand the core concept. That familiarity is an advantage most Texas buyers do not have. The key adjustment: the 10% homestead cap limits annual increases but still allows significantly more exposure than Proposition 13. A MUD tax on a $750,000 home today could become a MUD tax on an $825,000 home in a single year if the market appreciates 10% — and that growth compounds year after year.

When you see a listing that mentions a MUD or PID, you already know to ask the right questions. For a full walkthrough, see How to Find Special Districts — Step by Step.

Key Takeaway

California Mello-Roos taxes and Texas MUD taxes are closely analogous. PID assessments work differently: they are special assessments structured as annual installments plus interest. The critical adjustment is that Texas's appraisal cap is substantially weaker than Proposition 13. Use your California knowledge to evaluate Texas properties with confidence, but model your long-term costs with the understanding that both the rate and the assessed value can change annually.

MUD vs. PID: What Is the

Difference?

MUDs and PIDs are structurally different — not just different names for the same thing. A MUD is an independent taxing authority that levies ad valorem taxes, while a PID is created by a city or county and imposes special assessments (not taxes). Both add to your monthly cost, but they fund different things, operate on different timelines, and carry different implications for your long-term housing expense.

MUD taxes tend to be long-term or permanent obligations. PID assessments have multiple components — capital assessments, bond installments, and ongoing service assessments — each with its own duration and terms. Always verify the specifics through the district's documents.

| Feature | MUD — Municipal Utility District | PID — Public Improvement District |

|---|---|---|

| What it funds | Water supply, wastewater/sewer, drainage, roads, and core infrastructure | Public improvements including infrastructure (roads, drainage, utilities) as well as neighborhood enhancements (landscaping, lighting, parks, trails, sidewalks) |

| Why it exists | To build infrastructure in areas where no municipal water, sewer, or roads exist — typically new subdivisions on previously undeveloped land | To fund public improvements — infrastructure, roads, drainage, utilities, and neighborhood enhancements — for a specific area, as authorized by the city or county that created it |

| Legal mechanism | Ad valorem property tax — an independent government taxing authority levying taxes based on appraised value, subject to appraisal-district oversight | Special assessment (not an ad valorem tax) — annual installments plus interest and administrative costs, imposed on properties within the district, administered by the city or county that created it. Not an independent taxing authority. |

| Typical rate | $0.25 to $1.50 per $100 of taxable value | Varies by community — no statewide typical rate. Assessed per the property's Service and Assessment Plan using frontage, square footage, property value, or other benefit-based apportionment methods. |

| Annual cost on a $750K home | $1,875 to $11,250 per year | See the property's actual assessment roll or Service and Assessment Plan for the specific annual amount — cost varies by property and apportionment method. |

| Duration | Long-term — bonds typically repaid over 20–30 years, but new bonds can be issued; in practice, many MUDs have no clear end date | Varies by assessment type — terms differ widely and can extend much longer than buyers expect. Bond-financed capital assessments may have a defined repayment term; ongoing service/maintenance assessments may have no fixed expiration. Assessments are paid in annual installments plus interest, may vary annually, and outstanding balances can be prepaid. |

| Can it be extended? | Yes — new bonds can sustain or increase the tax rate, especially in multi-phase developments | Duration depends on the service and assessment plan, annual updates, and bond documents — not a fixed statutory expiration. Texas law permits assessments to vary annually, so the dollar amount may change from year to year. |

| Key difference for resale buyers | A resale home in a MUD may still carry 10–20+ years of bond debt. The tax burden does not reset when the home changes hands. | A resale home in a PID may still carry active assessment obligations — and assuming the PID has expired based on its age or the home's resale status is a common mistake. Different components of the assessment (capital, bond installments, and ongoing service assessments) each have their own duration, and some may continue indefinitely. Outstanding PID assessments can also be prepaid at closing. |

| What to verify | Outstanding bond amount, remaining bond term, and whether additional bonds are planned | Current service and assessment plan, annual assessment roll, bond documents (for outstanding bonds), and whether ongoing service assessments have no expiration |

A MUD tax is more likely to be a long-term or permanent layer on your tax bill, because the district can refinance and issue new bonds. A PID's structure is fundamentally different — special assessments paid in annual installments plus interest.

Key Takeaway

MUDs are independent taxing authorities that fund infrastructure and typically carry long-term bond obligations. PIDs are created by a city or county and fund public improvements through special assessments — not ad valorem taxes. When evaluating a resale home, ask: What does the current service and assessment plan say about each assessment component's duration?

How Bond Debt Turns Into

Your Monthly Payment

To understand why special districts move your monthly payment, you need to understand one mechanism: municipal bond financing.

When a developer builds a new Hill Country subdivision, the infrastructure — water lines, sewer connections, drainage systems, roads, and sometimes parks and amenities — must be built before the first home closes. The cost can run millions of dollars.

Rather than absorb that cost entirely, the developer works with the state to create a special district. In the case of a MUD, the district issues tax-exempt municipal bonds to reimburse the developer for the infrastructure costs.11 In the case of a PID, the city or county that created the district funds improvements through special assessments imposed on properties within the district — annual installments plus interest and administrative costs — rather than through bond-backed ad valorem taxes.

A MUD repays those bonds over a term of 20 to 30 years using property taxes levied on every property owner within the district boundaries. This bond repayment is in addition to the base county, school, and city taxes. It appears on your tax bill as a separate line item — often labeled "debt service" or "MUD bond repayment." The bond repayment portion is the I&S (interest and sinking) component of the MUD rate. See MUD Rate Breakdown: M&O vs. I&S for how the total MUD rate splits between operations and debt service.

The critical insight is this: the bond debt portion of your MUD tax bill is a separate levy that can sometimes equal or exceed the base tax rate itself. In a newly developed subdivision where bonds are freshly issued and at their highest outstanding balance, the MUD bond debt service can represent $0.50 to $1.50 per $100 of taxable value — effectively doubling the tax rate you expected. PID assessments, by contrast, are special assessments (not ad valorem taxes) and carry their own installment-based structure.

For resale buyers: The bond debt does not retire when the original buyer sells. A resale price that seems competitive may carry a tax burden that makes the true monthly cost significantly higher than a comparable home outside the district — always check the remaining bond term.

How a Combined Tax Rate Is Assembled

Illustrative example: $750,000 home in a Hill Country development with MUD + ESD. Rates per $100 of taxable value (shown here at full appraised value before exemptions). This applies equally whether the home is new construction or resale. Hypothetical illustration

Why a Lower Rate Doesn't

Mean a Lower Bill

This is one of the most dangerous half-truths in Texas real estate. The bond debt section above explains that MUD tax rates may decline over time as bonds are paid off — but that is not guaranteed, because new debt, changing valuations, and altered repayment schedules can offset or reverse the trend. And even when the rate does decline, a declining rate does not guarantee a declining tax bill — and in fast-appreciating Hill Country markets, it often does not.

How Texas Assessed Values Work

Texas Appraisal Districts — including the Kendall County Appraisal District, Bexar County Appraisal District, and Comal County Appraisal District — are required by law to reappraise all property at least once every three years at 100% of their current market value.19 This is not optional. The appraisal district determines what your home is worth on the open market at least once every three years — and in practice, most Hill Country CADs appraise property more frequently. But your property tax is not calculated on that appraised market value — it is calculated on the taxable value, which is the appraised value after the application of appraisal caps, exemptions, and any special valuations. Each taxing entity applies its own adopted rate to the property's taxable value for that entity, and the taxable value can differ from one entity to another depending on which exemptions each entity honors.

The formula for each taxing entity is: Tax = Taxable Value × That Entity's Adopted Rate. Both variables can change every year. The taxable value is derived from the appraised value after any applicable caps, exemptions, and special valuations — so the number being multiplied by the rate is usually lower than the appraised market value. If the rate goes down but the taxable value goes up faster, the dollar amount you owe goes up. The rate is only half the equation — and it's the half that most people fixate on while ignoring the other.

The Proposition 13 Gap

This dynamic is particularly jarring for California relocators. Under Proposition 13, your assessed value is locked at purchase price with annual increases capped at 2%.20 In Texas, qualifying homesteads receive a 10% annual cap — not 2%, not locked to acquisition value. Non-homestead properties face only a temporary 20% cap for properties valued at $5 million or less (expiring December 31, 2026), and properties above $5M receive no cap. A home that appreciated 23.5% in three years could see its appraised value increase by 10% per year under the homestead cap, meaning the tax bill still rises substantially even with the protection in place.

A Worked Example

Consider a buyer who purchases a home in a MUD in 2025 for $425,000. The local appraisal district determines the property's market value as of January 1 — the purchase price is one data point the CAD considers, but it does not automatically become the appraised value, particularly in Texas where the CAD may not have the exact sale price. For this example, suppose the CAD appraises the property at $425,000. Because this is the first year of ownership and no exemptions have yet been applied, the property's taxable value for the MUD equals the appraised value of $425,000 (most MUDs have not adopted a local-option homestead exemption). The MUD debt service (I&S) tax rate is $0.85 per $100 of taxable value. Note: this is the I&S (interest and sinking) component only — the M&O (maintenance and operations) rate is a separate, ongoing charge. See M&O vs. I&S above.

| Initial Assessment (2025) | Three Years Later (2028) | |

|---|---|---|

| Taxable Value (MUD) | $425,000 | $525,000 |

| MUD Rate (per $100) | $0.85 | $0.70 |

| MUD Tax Owed | ~$3,613/yr | ~$3,675/yr |

| Rate Change | — | ↓ 17.6% decrease |

| Bill Change | — | ↑ Higher, not lower |

The MUD rate dropped by 17.6% as bonds were paid down — exactly what the bond schedule promised. But the home's assessed value rose from $425,000 to $525,000 — a 23.5% increase over three years — which is realistic for fast-growing corridors like Boerne and Fair Oaks Ranch where Hill Country demand has been relentless. The result: the homeowner's MUD tax increased by roughly $62 per year despite a substantially lower rate.

And that is only the MUD portion. The school district rate — typically the largest single component of the tax bill — is applied to the same market-value assessment. If Boerne ISD or Comal ISD rates hold steady while the home appreciates, that portion of the bill rises too. The county portion follows the same logic. A declining special-district rate may reduce the total combined tax rate, but if every other component is applied to a higher assessed value, the net effect can still be a larger annual bill.

What This Means in Practice

A buyer who purchases based on today's MUD rate and today's assessed value may face a meaningfully higher tax bill within two to three years if the area appreciates rapidly — which is common in Hill Country growth corridors. The rate trajectory looks favorable on paper. The bill trajectory does not follow.

This is not a flaw in the system. It is how Texas property tax is designed to work. The appraisal district's job is to reflect market reality, and the market in much of the Hill Country has been appreciating faster than bond rates are declining.

Key Takeaway

- •Rate contraction does not equal tax bill contraction. Your tax bill is the product of assessed value multiplied by the rate — if value rises faster than the rate falls, you owe more.

- •Always project your tax trajectory based on both the rate trend and the local appreciation trend — not just today's rate.

- •Ask your agent or tax advisor to model a three-to-five year projection using both declining rates and increasing assessed values — especially important for California relocators accustomed to Proposition 13's 2% cap.

The Monthly Payment Impact:

Four Scenarios, One Home Price

The following examples use a $750,000 home — a realistic price point for Hill Country and Boerne-area properties — with realistic combined tax rate ranges for each scenario. Scenarios 1–3 apply to both new construction and resale purchases. Scenario 4 illustrates a common resale situation where the MUD has partial bond debt remaining.2

Understanding Tax Exemptions

The table below uses pre-exemption values — the full tax calculated on the entire appraised value without exemptions. Most homeowners qualify for at least one exemption and will pay less. Here are the key exemptions:

- •Homestead Exemption: Reduces the school district portion by up to $140,000 off appraised value. Counties and cities may offer additional reductions.12

- •Over-65 / Senior Exemption: An additional $60,000 school district exemption (total $200,000), plus a school district tax ceiling that caps the annual school tax bill at the amount owed when the exemption was claimed.13

- •Disabled-Person Homestead Exemption (§11.13): Available to individuals who qualify for federal Social Security disability insurance (SSDI). The federal government determines who qualifies as disabled; taxing units may choose whether to adopt the exemption and at what amount, but they do not set separate eligibility criteria. Separate from the disabled-veteran exemption — different statute, different application process.14

- •Disabled-Veteran Homestead Exemption (§11.22): Scales with VA disability rating — $5,000 (10%–29%), $7,500 (30%–49%), $10,000 (50%–69%), $12,000 (70%–99%). A full exemption under §11.131 is available for veterans receiving 100% VA disability compensation with a 100% rating or IU determination.15

- •Agricultural / Wildlife Valuation: Taxes land based on productive use rather than market value. Less common in typical residential purchases but relevant for rural acreage.

Note: The disabled-person exemption (§11.13) and the disabled-veteran exemption (§11.22/§11.131) are separate programs with different statutes, eligibility criteria, and application processes. The disabled-person exemption requires qualifying for federal Social Security disability insurance (SSDI); the disabled-veteran exemption requires a VA disability rating. A VA disability rating does not qualify someone for the disabled-person exemption; an SSA disability determination does not qualify someone for the disabled-veteran exemption.

The same assessed value, two very different tax bills. The difference is entirely driven by which special taxing districts apply to the property.

| Tax Component | Scenario 1 No Special Districts | Scenario 2 MUD + ESD | Scenario 3 MUD + PID + ESD | Scenario 4 Resale in MUD (partial bonds remain) |

|---|---|---|---|---|

| Ad Valorem Tax Rates (per $100 of taxable value) | ||||

| County | $0.32 | $0.32 | $0.32 | $0.32 |

| School District | $0.92 | $0.92 | $0.92 | $0.92 |

| MUD | — | $0.70 | $0.70 | $0.45 |

| ESD | — | $0.08 | $0.08 | $0.08 |

| Ad Valorem Subtotal | 1.24% | 2.02% | 2.02% | 1.77% |

| Annual Ad Valorem Tax | $9,300 | $15,150 | $15,150 | $13,275 |

| Non-Ad Valorem Special Assessments (flat annual $) | ||||

| PID Assessment | — | — | $1,875/yr | — |

| Non-Ad Valorem Subtotal | $0 | $0 | $1,875 | $0 |

| Combined Annual Cost (Ad Valorem + Special Assessments) | ||||

| Total Annual Cost | $9,300 | $15,150 | $17,025 | $13,275 |

| Monthly Cost (pre-exemption) | $775 | $1,263 | $1,419 | $1,106 |

Ad valorem rates are per $100 of taxable value. In this pre-exemption illustration, the taxable value for each entity equals the full $750,000 appraised value. In practice, exemptions (such as the $140,000 school district homestead exemption) reduce the taxable value for each entity independently. Annual ad valorem taxes = rate × $7,500.

PID Assessment: PID assessments are special assessments — not ad valorem taxes — structured as annual installments plus interest and administrative costs. The $1,875/yr for Scenario 3 is an illustrative annual amount based on a $750,000 home. PID assessments are allocated by benefit-received matrix or fixed square-footage/lot allocation — they are not tax rates and are not subject to homestead exemptions. Texas law permits assessments to vary annually, and outstanding balances can be prepaid. Buyers should confirm with the title company or PID administrator what the current assessment is, how it is allocated, and how it may change.

The same $750,000 home produces monthly tax bills ranging from $775 (no special districts) to $1,419 (MUD + PID + ESD) — a difference of $644 per month driven entirely by which districts tax the property. Even a resale in a MUD with partially retired bonds (Scenario 4) adds $331 per month over the baseline, because the M&O (operations) rate continues regardless of bond repayment.

The homestead exemption reduces the school district portion of these numbers, but does not reduce the MUD, ESD, or PID layers — those entities rarely adopt local-option homestead exemptions, and PID assessments are special assessments (not ad valorem taxes) that are not subject to homestead exemptions at all.

Purchasing Power and Resale Impact

This tax difference directly reduces how much home you can afford. A buyer pre-approved at $5,200/month may qualify for an $850,000 home without special districts, but only a $745,000 to $770,000 purchase in a MUD + PID + ESD area.

When you eventually sell, informed buyers will run the same analysis. A home with $600+/month in special-district costs has a narrower pool of qualified buyers — a real consideration for long-term ownership.

Key Takeaway

Two homes priced identically at $750,000 can produce monthly tax bills that differ by $488 to $644 or more — purely based on which special taxing districts apply. That gap compounds over the life of your loan and directly reduces your purchasing power. Resale does not automatically mean lower special-district taxes; the remaining bond term matters more than the age of the home.

Three Hill Country Case Studies

The scenarios above show the impact of special districts. These three case studies show the mechanics — the three separate value numbers on your tax bill (market value, appraised value, and taxable value), how exemptions work, and how the math produces your actual dollar amount. Each case uses realistic Hill Country values in the $725,000 to $775,000 range and current published tax rates.

Case Study 1: Property WITHOUT a Special District

Kendall County, outside city limits, Boerne ISD and Cow Creek GCD

This is the cleanest tax structure in the Hill Country, and when you find one, it's a good day. You purchase a resale home in Kendall County outside any city limits. The property is taxed by Kendall County, Boerne ISD, and the Cow Creek Groundwater Conservation District only. No MUD, no PID, no ESD.

Step 1: The Three Value Numbers

- •Assumed purchase price and CAD market value: $775,000.

- •Appraised value (assessed value): $775,000 — the county appraisal district's determination of market value as of January 1. In year one, the CAD appraises the property at its estimate of market value; your purchase price may be one piece of evidence but does not automatically set the appraised amount (Texas is a nondisclosure state). In this example, the appraised value matches the purchase price.

- •Taxable value: The appraised value minus your exemptions. This is the number each taxing entity actually applies its rate to.

Step 2: Apply Your Exemptions

You qualify for the standard homestead exemption (you will use this as your primary residence).

- •School district taxable value: $775,000 − $140,000 (homestead) = $635,000

- •County taxable value: $775,000 (Kendall County shows no general homestead exemption in the 2025 official rate table)

Step 3: Calculate Each Tax

Kendall County: $775,000 × 0.377% = $2,922

Boerne ISD: $635,000 × 1.0109% = $6,419

Cow Creek GCD: $775,000 × 0.005% = $39

Total estimated annual tax: $9,380

Monthly: $782

Effective Rate Summary

Combined tax rate (county + ISD + Cow Creek GCD): 1.3929%

Effective rate (total tax ÷ market value): 1.21%

The effective rate is lower than the combined rate because the $140,000 school district homestead exemption reduces the taxable base for ISD taxes below the $775,000 market value.

No special districts. No surprises. A combined rate of 1.3929% — about the lowest you will find in the Hill Country — translates to a monthly tax of $782. This is the baseline that Case Studies 2 and 3 are measured against.

Case Study 2: MUD Property in Kendall County

Kendall County, Boerne ISD, Cow Creek GCD, Kendall County MUD #1

You purchase a new-construction home in a master-planned community within Kendall County MUD #1. The MUD issues ad valorem taxes to repay infrastructure bonds. The published total MUD rate is $0.65 per $100 of taxable value — see M&O vs. I&S above for how MUD rates typically split between operations and debt service.

Step 1: The Three Value Numbers

- •Market value: $725,000

- •Appraised value: $725,000 (year one — no cap has built up yet)

- •Taxable value: $725,000 minus your exemptions (see below)

Step 2: Apply Your Exemptions

- •School district taxable value: $725,000 − $140,000 = $585,000

- •County taxable value: $725,000 (no Kendall County general homestead exemption per 2025 official table)

- •Cow Creek GCD taxable value: $725,000 (no homestead exemption)

- •MUD taxable value: $725,000 (MUDs rarely adopt local-option percentage homestead exemptions; when they do, the exemption applies across the entire MUD levy. The full appraised value is used because most MUDs have not exercised this option)

Step 3: Calculate Each Tax

Kendall County: $725,000 × 0.377% = $2,733

Boerne ISD: $585,000 × 1.0109% = $5,914

Cow Creek GCD: $725,000 × 0.005% = $36

Kendall County MUD #1: $725,000 × 0.65% = $4,713

Total estimated annual tax: $13,396

Monthly: $1,116

MUD Delta: What the MUD Actually Costs You

To see the true cost of the MUD, compare this home to a hypothetical $725,000 home in the same county and school district but without a MUD:

Without MUD: Kendall County $2,733 + Boerne ISD $5,914 + Cow Creek GCD $36 = $8,683/yr ($724/mo)

With MUD: All layers combined = $13,396/yr ($1,116/mo)

The MUD adds $4,713 per year — $393 per month

Effective Rate Summary

Combined tax rate (county + ISD + Cow Creek GCD + MUD): 2.0429%

Effective rate (total tax ÷ market value): 1.85%

The MUD raises the combined rate by 0.65 percentage points — from 1.3929% (baseline) to 2.0429%. On a $725,000 home, that 0.65% translates to $4,713 per year in additional tax.

The MUD adds $4,713 per year — $393 per month — on top of the base county, school, and groundwater conservation district taxes. The MUD alone raises the combined tax rate from 1.3929% to 2.0429%. On a $725,000 home, that is the difference between a $724/month tax bill and a $1,116/month tax bill — a 54% increase in your monthly tax obligation. The published total MUD rate ($0.65 per $100) reflects the combined effect of operations and debt service. As bonds are repaid, the debt-service portion of the rate may decrease — but MUDs can also issue new bonds for additional infrastructure, which can sustain or increase the total rate. The M&O component continues as long as the district provides services.

Case Study 3: Unincorporated Bexar County with PID

Unincorporated Bexar County, Boerne ISD, with PID assessment — no MUD

This scenario reflects what many buyers encounter in the Boerne-area communities that extend into Bexar County — unincorporated parcels within Boerne ISD boundaries that fall under Bexar County's taxing authority. The property sits in a master-planned community with a Public Improvement District — created by the city or county — that funds public improvements including infrastructure and neighborhood enhancements such as landscaping, parks, lighting, and trail maintenance. There is no MUD, so you can see the PID's cost layered directly onto an illustrative six-entity Bexar County stack.

Unlike Case Study 1 (Kendall County, where only three entities tax the property), a Bexar County parcel carries six separate taxing entities — even without a MUD or groundwater conservation district.

Step 1: The Three Value Numbers

- •Market value: $775,000

- •Appraised value: $775,000 (year one)

- •Taxable value: $775,000 minus your exemptions — and each entity applies its own exemption (or none) independently

Step 2: Apply Your Exemptions

- •School district (Boerne ISD) taxable value: $775,000 − $140,000 (state mandatory homestead) = $635,000

- •Bexar County taxable value: $775,000 − $155,000 (Bexar County's optional 20%-or-$5,000 homestead exemption — 20% of $775,000 = $155,000, which exceeds the $5,000 floor) = $620,000

- •Road & Flood Control: $3,000 plus 20% of appraised value — $3,000 + (20% × $775,000) = $158,000 exemption → taxable value $617,000

- •Alamo Colleges: $5,000 or 1% of appraised value (greater of the two) — 1% × $775,000 = $7,750, which exceeds $5,000 → taxable value $767,250

- •University Health: $5,000 or 20% of appraised value (greater of the two) — 20% × $775,000 = $155,000, which exceeds $5,000 → taxable value $620,000

- •San Antonio River Authority: $5,000 or 4% of appraised value (greater of the two) — 4% × $775,000 = $31,000, which exceeds $5,000 → taxable value $744,000

Step 3: Calculate Each Ad Valorem Tax

Six entities tax this property. Here is each entity, its 2025 adopted rate, the applicable taxable value, and the resulting tax:

Bexar County: $620,000 × 0.276331% = $1,713

Road & Flood Control: $617,000 × 0.023668% = $146

Boerne ISD: $635,000 × 1.0109% = $6,419

Alamo Colleges: $767,250 × 0.149150% = $1,144

University Health (Hospital District): $620,000 × 0.276235% = $1,713

San Antonio River Authority: $744,000 × 0.0183% = $136

Ad valorem total (outside San Antonio): $11,272

The county rate ($0.276331) and Road & Flood rate ($0.023668) are from the 2025 Bexar County Tax Assessor-Collector's published rate table. Boerne ISD's $1.0109 rate was voter-approved November 4, 2025. Alamo Colleges ($0.149150), University Health ($0.276235), and SARA ($0.0183) are from the 2025 adopted rates. The homestead exemptions above reflect the official 2025 Bexar County exemptions: Bexar County uses 20%-or-$5,000 (greater) while Road & Flood Control uses $3,000 plus 20% of appraised value, Alamo Colleges uses $5,000-or-1%, University Health uses $5,000-or-20%, and SARA uses $5,000-or-4%. Note: this estimate excludes any Emergency Services District (ESD) that may apply to the actual property address, as well as any groundwater conservation district — Cow Creek GCD, for example, is a Kendall County entity that does not levy taxes on Bexar County parcels.

Inside San Antonio City Limits: One Additional Entity

If the same property were located inside San Antonio city limits, the City of San Antonio would add a seventh taxing entity. The City's 2025 adopted rate is $0.54159 per $100, and it offers a homestead exemption of 20%-or-$5,000 (greater).

City of San Antonio: ($775,000 − $155,000) × 0.54159% = $620,000 × 0.54159% = $3,358

Ad valorem total (inside San Antonio): $11,272 + $3,358 = $14,630

With assumed PID assessment ($2,100): $16,730/yr ($1,394/mo)

The City of San Antonio rate is from the city's adopted 2025 fiscal year tax rate. The seven-entity stack inside city limits adds roughly $3,358 per year — the equivalent of $280 per month — on top of the six-entity unincorporated total.

Step 4: Add the PID Assessment

PID assessments are structured as annual installments plus interest and administrative costs — not an ad valorem rate. Texas law permits assessments to vary annually. For illustration, assume a PID that charges a capital assessment plus an annual maintenance assessment:

PID capital assessment (annual installment): $1,500

PID maintenance assessment (landscaping, lighting, trails): $600

Total PID assessment: $2,100/year

Step 5: Total Estimated Annual Cost

Ad valorem taxes (all six entities, outside SA): $11,272

PID assessment: $2,100

Total estimated annual tax + assessment: $13,372

Monthly: $1,114

PID Delta: Illustrative PID Cost Impact

Compare this home's ad valorem cost to the PID-inclusive total:

Without PID: Ad valorem only = $11,272/yr ($939/mo)

With PID: Ad valorem + PID = $13,372/yr ($1,114/mo)

The PID adds $2,100 per year — $175 per month

Effective Rate Summary

Combined ad valorem rate (all six entities, before exemptions): 1.7546%

Effective rate (ad valorem only ÷ market value): 1.454%

Effective rate (ad valorem + PID ÷ market value): 1.725%

The combined rate (1.7546%) reflects six overlapping entities — more than double the three-entity stack in Case Study 1 (Kendall County). At the same $775,000 market value, the effective rate (1.454%) is higher than Case Study 1's effective rate (1.21%) and even exceeds its combined rate (1.3929%), and that is before an assumed $2,100 PID assessment is added. Inside San Antonio city limits, the effective rate rises to approximately 1.888% (or 2.159% with the assumed PID) once the City of San Antonio tax is included.

The full Bexar County entity stack is $11,272 before any special district — compared to $9,380 in Kendall County (Case Study 1). At the same $775,000 market value, the ad valorem tax difference between the two counties is roughly $1,892 per year — entirely driven by the six-entity Bexar County stack versus the three-entity Kendall County stack. The PID adds an assumed $2,100 on top. Inside San Antonio city limits, the City of San Antonio tax adds another $3,358, bringing the seven-entity total to $14,630 ($16,730 with the assumed PID). Review the PID Due Diligence Checklist below for the documents to request.

Key Takeaway

Three separate value numbers — market value, appraised value, and taxable value — determine your tax bill. A $775,000 home with county, school, and Cow Creek GCD taxes pays $9,380 per year ($782/mo). Add a MUD, and a $725,000 home pays $13,396 ($1,116/mo) — the MUD alone adds $4,713 per year. In Bexar County, six entities stack onto the same $775,000 home — $11,272 per year before any special district. Add a PID, and the total reaches $13,372 ($1,114/mo) — the PID adds an assumed $2,100 per year as a flat assessment. At the same market value, the Bexar County six-entity stack costs roughly $1,892 more per year than the Kendall County three-entity stack — location alone, no special districts. Inside San Antonio city limits, the City of San Antonio tax pushes the seven-entity total to $14,630 ($16,730 with the assumed PID, or $1,394/mo). Each entity's own homestead exemption reduces its taxable value independently — the savings add up across all six (or seven) entities. The math is transparent once you know which numbers to use.

Downloadable Worksheet

Use the Tax Estimation Worksheet (printable HTML) to calculate your estimated taxes by jurisdiction and by your own exemptions. The worksheet includes fields for market value, appraised value, exemptions, each entity's rate, total estimated tax, and MUD/PID assessments. Print it, fill it out for each property you are evaluating, and bring it to your lender consultation.

Download Tax Worksheet

The DTI Trap: How Special

Districts Can Derail Your Mortgage

Special district taxes do not just stretch your budget — they can determine whether you qualify for a mortgage at all. This is the section that most buyers, and many agents, overlook entirely.

How Lenders Use Taxes in Your Qualification

The lender calculates your Debt-to-Income ratio (DTI) using the full PITI: Principal, Interest, Taxes, and Insurance. Most conventional lenders want this number at or below 43%–45%.

The "T" in PITI is based on the actual projected property tax bill — county, school district, city, and any special districts. PID assessments must also be included in your monthly housing cost. A higher total tax bill means the lender qualifies you for a smaller loan — or may determine you cannot qualify at all.

The Real-World Danger: Failing Underwriting at Closing

Consider a buyer earning $13,000 per month (gross) with $400 per month in other recurring debt, purchasing a $750,000 home with 20% down ($600,000 loan at 7.0%).

Baseline rate (no special districts): approximately 1.80%. Annual tax: $13,500. Total PITI: $5,392/month.

With MUD + PID layers (tax-and-assessment equivalent of approximately 2.85%): Annual tax: $21,375. Total PITI: $6,048/month. That $656/month difference is the combined special district surcharge — enough to move the DTI from a plausible conventional approval to a range where most lenders will decline.

What Special District Taxes Do to a DTI Calculation

Baseline assumptions: $750,000 purchase, 20% down ($150,000), $600,000 loan at 7.0% / 30-year fixed (P&I: $3,992/mo), $275/mo homeowner's insurance, $13,000/mo gross income, $400/mo other debt.

| Scenario | Monthly P&I | Tax & Assessment | Total Housing + Debt | Back-End DTI |

|---|---|---|---|---|

| No special district | $3,992 | $1,125/mo ($13,500/yr) | $5,792 | 44.6% |

| MUD + PID | $3,992 | $1,781/mo ($21,375/yr) | $6,448 | 49.6% |

Tax-and-assessment rates: baseline ~1.80% (county + school + city); MUD + PID ~2.85% tax-and-assessment equivalent including MUD ad valorem plus PID special assessments.

The delta: $656 per month in additional housing cost and 5.0 percentage points on the DTI — the difference between a plausible conventional approval (~44.6%, within the typical 43%–45% target) and a level (~49.6%) where most conventional lenders will decline or require significant compensating factors.

Calculated using standard 30-year amortization on a $600,000 loan at 7.0%. Rates and qualifying thresholds vary by lender and loan program.

If this is discovered late, the buyer has two layers of contractual protection: the option period (typically 7 to 14 days, allowing termination for any reason — lose only the option fee) and the financing contingency (TREC Third Party Financing Addendum — which separately addresses buyer approval, property approval, deadlines, and notice requirements — review the specific terms of your completed addendum with your agent or attorney). Both have expiration dates. Earnest money at stake is typically 1%–2% of the purchase price — $7,500 to $15,000 on a $750,000 home.

New Construction Is Especially Risky

Builders often quote payment estimates using initial MUD rates and PID assessment amounts that can change. The builder's estimated payment may not reflect the full tax burden at closing — or after the first post-construction reassessment. Buyers who rely solely on the builder's estimate may find themselves unable to qualify once the actual tax bill is calculated.

After closing, the lender conducts an annual escrow analysis: if property taxes or homeowner's insurance have increased, your monthly escrow payment goes up to cover the shortfall, and your total monthly housing payment (PITI) rises accordingly. This is a cash-flow change, not a loan modification — your interest rate and principal/interest payment remain locked for the life of a fixed-rate mortgage. Critically, the lender does not re-run your debt-to-income ratio during this annual escrow analysis. Your DTI is only recalculated when you apply for new financing — refinance, home equity loan, or other credit. A buyer who barely qualified at closing may find themselves above the DTI threshold the next time they apply for new financing, even though the lender never reassessed their DTI in the interim.

What I Tell Every Client to Do

Run Pre-Approval With Full Tax Rates

Ask your lender to calculate your pre-approval using the full current tax rate, including all special districts — not just county and school district. If the lender's pre-approval letter does not account for MUD taxes or PID assessments, the qualification number may be wrong.

Get Rates in Writing

Ask the builder or title company for the exact current MUD tax rates and PID assessment rates and have your lender recalculate your DTI with those numbers.

Verify During Your Option Period

Verify the exact taxing jurisdictions — the title company can provide this — and ask your lender to re-run your numbers. The mandatory MUD and PID disclosures should surface this information early, but do not assume they will. Confirm independently.

Get Written Confirmation From Your Lender

Get your lender to confirm in writing that the DTI calculation includes the full current tax rate for every jurisdiction. A verbal "it should be fine" is not underwriting.

Key Takeaway

A MUD tax or PID assessment layer of $656 per month or more can push you above your DTI threshold and disqualify you from a loan. Always have your lender calculate qualification using the full, current tax rate including all special districts — and use your option period and financing contingency early, not at the last minute.

Escrow Shortages: Why Your

Monthly Payment May Go Up

After you close, the lender's annual escrow analysis compares the actual tax bill to what was collected. If the actual bill is higher — due to new construction reassessment, seller exemptions you don't qualify for, incomplete exemption filing, or a rate increase — the lender notifies you of a shortage and raises your monthly payment, sometimes by $150 to $400 or more. This is one of the things I warn every client about up front: your payment at closing may not be your payment six months later.

How to Prepare

- •Budget for a first-year increase. Plan for a potential 10% to 25% increase in your total housing payment, especially with new construction.

- •File your homestead exemption immediately. You can file with the county appraisal district as soon as you close.

- •Request a tax projection before closing. Ask your lender to model PITI using the full tax rate from all entities, not the seller's capped assessment.

- •Set aside reserves. Keep one to two months of additional tax cost in savings as a buffer.

Appraisal District vs.

Tax Assessor-Collector

The Appraisal District (CAD) appraises every property's value and maintains the tax rolls — it tells you what the property is worth and who taxes it. The Tax Assessor-Collector uses those values to calculate and collect your tax — it tells you how much you owe. File exemption applications and value protests with the CAD; request tax certificates and make payments through the Tax Assessor-Collector.

Hill Country Central Appraisal

District Directory

This is your starting point. Look up your property's appraised value, tax rates, and filing deadlines at your county's Central Appraisal District. I keep these bookmarks handy and reference them constantly. Each CAD maintains public records for every property in its jurisdiction — including ownership history, assessed values, exemptions on file, and the taxing entities that levy against the property.

Fair Oaks Ranch — Spans Three Counties

Fair Oaks Ranch is not located in a single county. Depending on the specific address, a property may fall under the jurisdiction of Kendall County, Bexar County, or Comal County — and therefore a different Central Appraisal District. You must determine which county your property is in before looking up tax records. The property address itself, or a quick search on any of the three CAD websites listed below, will tell you which district has jurisdiction.

Kendall County Appraisal District

Covers Boerne, Comfort, and unincorporated Kendall County (also parts of Fair Oaks Ranch — see note above)

Comal County Appraisal District

Covers New Braunfels, Canyon Lake, Spring Branch, and unincorporated Comal County (also parts of Fair Oaks Ranch — see note above)

Bexar County Appraisal District

Covers San Antonio, Helotes, Leon Valley, Shavano Park, and unincorporated Bexar County (also parts of Fair Oaks Ranch — see note above)

Hays County Appraisal District

Covers San Marcos, Dripping Springs, Kyle, Buda, Wimberley, and unincorporated Hays County

Bandera County Appraisal District

Covers Bandera, Lakehills, Medina, Pipe Creek, and unincorporated Bandera County

Medina County Appraisal District

Covers Hondo, Castroville, Devine, and unincorporated Medina County

Guadalupe County Appraisal District

Covers Seguin, Cibolo, Schertz, Marion, and unincorporated Guadalupe County

Key Takeaway

Your county's CAD is the first place to look when evaluating any Hill Country property. Search the address to find the property's current market value and appraised value (if the seller had a homestead cap, the appraised value may be lower than market value — use the market value as your planning baseline), every taxing entity that levies against the property (including MUDs and ESDs), and the applicable tax rates. PID assessments may not appear in CAD records (see Step 7 for PID-specific sources). File your homestead exemption with the same office after closing.

PID Due Diligence Checklist

If you are buying a property within a Public Improvement District, there are specific documents you should request and review before committing to a purchase. PIDs are more complex than MUDs because they can contain multiple assessment types — each with its own duration and terms. This checklist tells you exactly what to ask for and why.

Assessment Roll

Lists the specific dollar amount assessed against each property. Request the most recent version — the roll may be updated annually.

Service and Assessment Plan

A separate document adopted and updated by the PID's governing body — distinct from the original formation documents and assessment ordinance that established the district — specifying what improvements are funded, how assessments are calculated, the payment schedule, and the bond structure. The current SAP and its annual update are the most important operational documents for understanding how a PID's assessments work in practice.

Annual Update to the Service and Assessment Plan

The plan may be updated annually — assessment amounts, components, and terms can change. Always examine the current version, not the original filing.

Payoff Amount

The remaining balance you would pay to satisfy the obligation at closing. Capital assessments in some PIDs can be paid in a lump sum, reducing long-term carrying cost.

Continuing Maintenance Assessment

Covers recurring costs — landscaping, lighting, security, common-area upkeep. This assessment persists even after the capital assessment is paid off — it may continue after the capital assessment is paid and may have no fixed expiration.

Key Takeaway

PIDs may contain multiple assessment types, each with its own duration. Request all five documents above and review them before closing. If the seller cannot provide them, contact the city or county office that administered the PID creation directly.

What the Law Requires:

Mandatory MUD and PID Disclosures

Everything above is about identifying special district costs — asking the right questions, checking public records, and understanding what you are looking at. But there is a separate layer of protection that many buyers, particularly those relocating from out of state, do not know exists: Texas law requires the seller to disclose special district status to you in writing, before you are legally bound to the purchase.

If you are buying a home in Texas — whether new construction or a resale — and the property is within a Public Improvement District or a Municipal Utility District, the law entitles you to specific written notice before you sign a binding contract.

PID Disclosure — Texas Property Code § 5.014

Public Improvement Districts

Texas Property Code § 5.014 establishes a strict, mandatory disclosure requirement for residential real property located within a Public Improvement District. The requirements are unambiguous:

- The seller must provide the buyer with specific statutory written notice before a binding contract, identifying the PID by name and the assessment obligations.

- If the seller fails to provide this notice, the buyer may have termination rights — but timing, waiver, and exception provisions apply. Consult a Texas real-estate attorney regarding rights under a particular contract.

This is a meaningful protection — Texas law requires pre-contract disclosure, giving you the opportunity to evaluate these costs before you are committed.

MUD Disclosure — Texas Water Code § 49.452

Municipal Utility Districts

A parallel disclosure requirement exists for properties within a Municipal Utility District under Texas Water Code § 49.452. The statute requires that:

- The seller must provide written notice that the property is in a MUD, including the district's name, the existence and approximate amount of MUD taxes, and the nature of the district's authority to tax and issue bonds.

- Failure to provide this notice may affect the buyer's rights — but the statute contains timing, waiver, and exception provisions. Consult a Texas real-estate attorney regarding rights under a particular contract.

- MUD disclosures may also appear in TREC Form 59-0, purchase contract addenda, and the title commitment. However, the statutory requirement exists independently — the seller's obligation to disclose is triggered before the contract is signed, not at closing.

If a MUD tax shows up in the title commitment or closing documents but the seller did not disclose it before you agreed to buy, you may have rights — though timing, late disclosure, closing, and statutory exceptions can affect available remedies.

What This Means for You as a Buyer

If you do not receive that notice in a timely manner, you may have termination or damage rights under the statute — but these rights are not automatic. The statutes contain specific timing provisions, waiver provisions, statutory exceptions, and limitations on remedies. For MUD-type water district notices, closing after receiving late notice can waive both the right to terminate and the right to recover damages. If you received notice late or not at all, consult a Texas real-estate attorney regarding rights under a particular contract.

Always ask before you sign. Before entering a purchase contract, ask your agent or title company whether the property is in any special taxing districts, and confirm that the required statutory disclosures have been provided in writing. Do not wait for the closing process to surface this information — by then, you may have already waived your right to terminate on this basis.

New Construction:

Additional Considerations

New-construction buyers face a few additional nuances beyond the universal special-district dynamics. Texas law also requires the seller to disclose MUD and PID status in writing before you sign a binding contract — see mandatory disclosure requirements for details.

The "Year One" Tax Surprise

Before construction, the land is typically assessed at a lower value — often agricultural or unimproved land valuation. When the home is built and the land is reclassified, the assessed value jumps to reflect the new construction. Builders may quote a "tax estimate" based on pre-construction land values — that estimate can be dramatically lower than what you will actually pay once the county appraisal district reassesses the property at full market value with improvements.

Ag Valuation Roll-Back Tax Trap

The "Year One" surprise above mentions that the land's agricultural or wildlife valuation does not transfer to a residential buyer. What that bullet does not cover is the financial penalty triggered when you change the land's use: roll-back taxes.

When a buyer purchases land or a lot that currently holds an agricultural or wildlife valuation under 1-d-1 open-space agricultural or wildlife-management valuation under Subchapter D. Timberland under Subchapter E has related but separate rules. and changes the use to residential — or any non-qualifying use — the county appraisal district triggers roll-back taxes.23 This applies to all buyers of ag-valued or wildlife-valued land transitioning to residential use, with particular risk for buyers of acreage in brand-new developments or master-planned communities where the land recently held ag valuation.

How roll-back taxes work: The county recovers the tax savings the seller received from the ag valuation for the previous three years.23 The bill goes to whoever changes the use — typically the buyer or the developer, depending on the purchase contract. HB 3833 (2021) removed the statutory interest component for common 1-d-1 open-space and wildlife valuation rollback taxes, so the rollback generally recaptures the tax difference without automatic interest. Interest and penalties can arise only if the resulting bill becomes delinquent. Older 1-d agricultural valuation rules may differ.

The dollar amounts can be substantial. The rollback amount is the difference between what the land was taxed at under the ag valuation and what it would have been taxed at at market value, calculated across the preceding three tax years. On Hill Country acreage, that gap can easily run into thousands to tens of thousands of dollars depending on the acreage, the difference between the productive-use valuation and the market-value appraisal, and the applicable tax rates.

New developments are especially dangerous. In a brand-new subdivision or master-planned community, the developer's original land parcel may still carry an ag or wildlife valuation in the appraisal district's records. The developer may have already triggered the rollback by platting and beginning residential construction — or the buyer may trigger it upon taking possession and beginning residential use. Either way, the financial exposure is real and the timing is not always obvious.

What to do: Before closing on any rural or semi-rural lot, request a CAD verification of the property's current valuation status — confirm whether the parcel carries an ag or wildlife valuation. Address rollback liability explicitly in the purchase contract: specify in writing who bears the cost if a rollback is triggered. Do not assume the developer or the seller has already resolved it. A title company or real estate attorney can help ensure this language is included in your contract.

The "Split-Up" Valuation Delay for New Lots

The "Year One" surprise above addresses the jump from pre-construction land value to post-construction improved value. But there is a separate issue that affects buyers of newly subdivided lots: the split-up valuation delay.

When a developer plats a master lot into individual residential lots, the central appraisal district (CAD) needs time to assign individual parcel IDs and update its records. Until that processing is complete, the property may not have its own individual appraisal in the CAD system — the land may still appear under the developer's original blanket parcel. This means the taxable value your lender uses to set escrow may not reflect the eventual individual lot valuation.

What to do: Before closing, contact the relevant CAD directly to verify the property's current valuation status and confirm whether an individual parcel has been created and valued. Do not assume the CAD has processed the split-up simply because you have closed on the property. Ask your lender how escrow is being set while the individual parcel record is pending, and be prepared for the possibility that your escrow payment may be adjusted once the individual valuation is in place.

Builder Tax Estimates vs. Reality

Most builders provide a tax estimate on their price sheet or during the sales process. This estimate frequently reflects only the county and school district rates, without the full special district burden, or uses a pre-construction land value that will not survive the first post-construction reappraisal. Treat the builder's tax estimate as a starting point, not a final answer. Verify it against the actual tax bill of a comparable, already-closed home in the same development, and see How to Estimate Your Actual Tax Bill below for the step-by-step method.

MUD Rates Change Over Time

MUD tax rates are set annually based on the district's budget, outstanding bond debt, and operational needs. The I&S (debt service) portion may decline as bonds are repaid — but new bonds can be issued, especially in multi-phase developments, which can sustain or increase the rate. The M&O (operations) portion does not decline with bond repayment. For resale buyers, the trajectory is often more favorable, but always verify the actual bond schedule rather than assuming the rate will go down.

How to Find Out If a Property

Is in a Special District

Here is exactly how to identify special districts — step by step, with specific methods and a timeline you can follow. These are the concrete actions to take before you commit to a purchase.

Use the Hill Country Appraisal District Directory above to go directly to the correct county CAD website — every county in the region is listed with a direct link.

Quick Reference Checklist

Ask Your Buyer's Agent — and Know What to Ask

Ask your buyer's agent: "Is this property located in any special taxing districts — a MUD, PID, WCID, ESD, or road district?" Naming the district types matters. A general question like "Are there any extra taxes?" may not get a complete answer.

If your agent is unfamiliar with the area or new to Hill Country, do not rely on their guess. Verify independently using the remaining steps below. For out-of-state buyers, make sure your agent is licensed in Texas and familiar with the specific county's appraisal district — local expertise is not optional for this part of the process.

Check the County Appraisal District Website

This is where I always start